Why Court-Ordered Restitution Guarantees Financial Ruin for Ex-Felons

Most people assume that when you finish a federal prison sentence, your debt to society is paid. That is a myth. The reality is that the justice system attaches a financial anchor to your release that is nearly impossible to sever.

I understand the necessity of this system intimately. I served nearly a decade in federal prison for bank fraud. I owe restitution, and I fundamentally believe that victims must be compensated. But having lived inside the machinery of this debt, I can tell you that the federal restitution system is not actually engineered to make victims whole. It is engineered to guarantee financial ruin for those trying to rebuild their lives.

Where Do the Seized Assets Actually Go?

The financial bleeding begins the moment you are arrested.

In cases involving financial crimes, the government’s first move is typically to seize the defendant’s assets—homes, cash accounts, cars, and business equity. The stated goal is to liquidate these assets to repay the victims.

However, the government operates these liquidations in an absolute black box. Federal agencies routinely refuse to provide defendants with a transparent accounting of those sales. You have no way of knowing if your assets were sold for fair market value, or how much of that money actually reached the victims. As a result, you are released from prison carrying a massive, arbitrarily calculated debt, with zero transparency into how the government handled your life’s work.

Punished Before, During, and Long After Prison

The rules governing criminal justice debt defy basic economic survival. The government structurally ensures that you can never get ahead.

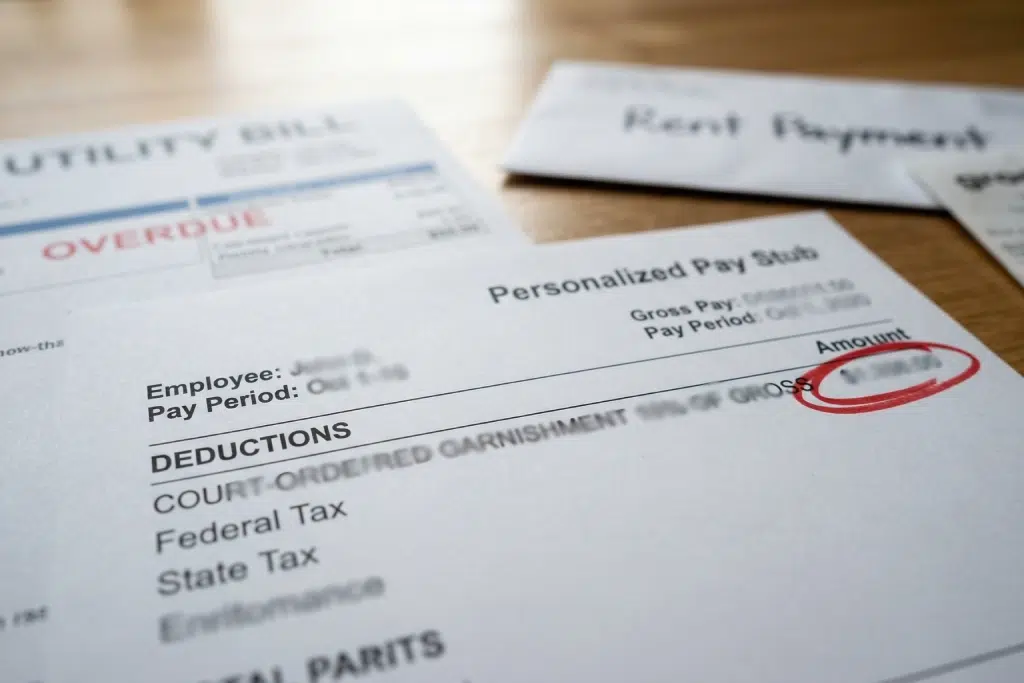

The drain starts while you are still locked up. Under the Inmate Financial Responsibility Program (IFRP), the government regularly seizes a portion of your prison commissary account—often taking between $25 and $100 a month. This policy actively strips inmates of the meager funds their families send them just to buy soap, toothpaste, or phone minutes to call their children.

Once you are released, the courts immediately target your wages. In my own case, the courts garnish 15% of my gross, pre-tax salary at the source. By the time taxes, rent, and food are accounted for, there is nothing left. If a 15% gross garnishment is crippling for a former executive, it is an absolute death sentence for someone re-entering society on minimum wage.

And there is no light at the end of the tunnel. Your restitution obligation does not run concurrently with your prison sentence. The mandatory 20-year clock for repayment only begins after you have completed your prison time and your supervised release. It operates as a lifetime financial sentence.

Designed to Fail: The Logistics of Paying the Court

Even the simple act of trying to hand the government your money is a bureaucratic nightmare.

In a modern, digital economy, you would assume you could easily wire your restitution payment to the court portal. You cannot. In jurisdictions like the Southern District of New York, individuals are required to physically submit cashier’s checks.

When you combine this with the banking blacklists I discussed in my previous post, the hurdle becomes absurd. If an ex-felon cannot legally open a bank account, how do they get a cashier’s check? They are forced to take time off from their fragile new job, travel to a check-cashing storefront, and pay exorbitant, predatory fees just to obtain the physical piece of paper required by the judge.

When Poverty Becomes a Parole Violation

The ultimate danger of this debt is how it weaponizes parole.

Recently released individuals are often forced to choose between paying their court-ordered restitution or paying their rent to avoid homelessness. If they choose to survive and cannot afford their restitution payment, their parole officer has the absolute authority to treat the missed payment as a supervision violation.

This exposes the individual to active warrants and direct re-incarceration. We have effectively recreated debtors’ prisons. We are sending people back to federal holding facilities not for committing new crimes, but because the math of their poverty didn’t add up.

About the Author

Hassan Nemazee operated in international finance before serving a federal prison sentence. Today, he advocates for pragmatic, economically focused systemic prison reform. He is presently on the board of directors for The Fortune Society.

Discover his full story in his memoir, Persia, Politics & Prison: A Life in Three Parts.

Frequently Asked Questions | Paying Restitution

Q.1. Do inmates have to pay restitution while they are still in prison?

A.1. Yes. In the federal system, the government regularly seizes funds from an incarcerated person’s commissary account to pay toward their restitution. This is often between $25 and $100 a month, draining funds meant for basic hygiene and communication.

Q.2. What happens if a person on parole cannot afford their restitution payment?

A.2. Failure to pay court-ordered restitution can be categorized by a parole officer as a supervision violation. This means an individual can face warrants, heightened wage garnishment, or be sent back to prison simply for being unable to afford the debt.

Q.3. Does the 20-year timeline to pay restitution include time served in prison?

A.3. No. The mandatory 20-year clock for repaying federal restitution does not begin until after an individual has fully completed both their prison sentence and their period of supervised release (probation).

Q.4. How do individuals make restitution payments to the court?

A.4. The system relies on archaic, high-friction methods. For example, in the Southern District of New York, individuals cannot wire payments; they are required to obtain and deliver physical cashier’s checks, which often requires taking time off work and paying extra banking fees.

")